Dollar Firm As Traders Brace For US Inflation

US Inflation Due

Markets have been bereft of tier-one US data over the last few weeks amidst the ongoing US shutdown. However, traders will today receive the first top-level US data since that shutdown with BLS releasing the September CPI figures after a 9-day postponement. Given the proximity to the upcoming October FOMC and likelihood that we don’t get any furtehr tier-one data beforehand, the release could fuel some volatility today if we see any surprise readings and will be closely watched.

Bullish USD Scenario

In terms of forecasts, the market is looking for headline annualised CPI to rise to 3.1% from 2.9% prior. With monthly core and headline readings both expected unchanged at 0.3% and 0.4% respectively. If seen, a rise in the headline data should keep USD supported near-term. While the Fed recently cited a shift in focus to the labour market, given the heavy weakness we saw in pre-shutdown data, inflation concerns were still noted as a threat. If inflation is seen rising again, particularly if we see an upside surprise today, this could dampen the more dovish forecasts we’ve seen. In this scenario, USD is likely to push higher into next week.

Bearish Scenario

However, if data surprises to the downside today, this could see a sharp unwinding of USD longs. Given the pre-shutdown weakness in the jobs market, a fresh decline in inflation will be seen as a greenlight for further Fed easing. The anticipated negative impact of the shutdown on the jobs market is also a factor to consider and the longer the shutdown persists, the greater the drag on jobs. In this scenario, USD could fall sharply today.

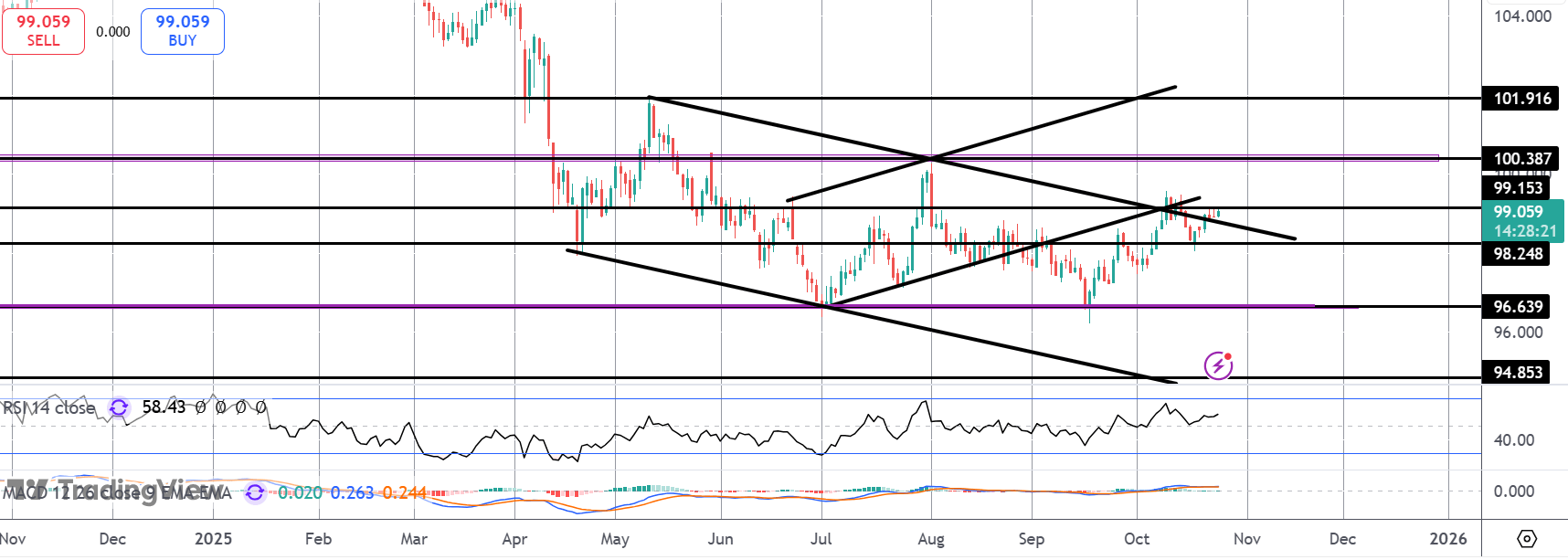

Technical Views

DXY

For now, DXY remains capped by the 99.15 level following the latest break of the bear channel highs. If we break higher today, the 100 mark will be the key hurdle for bulls with 101.96 the higher target to note. To the downside, 98.24 is the key support to watch.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.